Home » Articles posted by BoxClimber

Author Archives: BoxClimber

Top 10 Takeaways from VMworld 2016. Can VMware Deliver the Next Wave of Innovation?

VMworld 2016 General Session kicked off in Las Vegas on Monday morning with a sound of tribal drumbeats and a nice little poem loosely tied to the conference theme, be Tomorrow” The main presenter for the session was VMware CEO Pat Gelsinger – which was a change in style all previous events where former President and COO, Carl Eschenbach, has traditionally had hyper-energized approach to discussing VMware’s business and technology.

The General Sessions on Monday and Tuesday covered a lot of ground – below are the “Top 10 Takeaways from VMworld 2016”

-

Michael Dell’s Read My Lips moment: “No Changes to VMware Open Ecosystem”

One of the questions customers and VMware followers and partners have about the Dell acquisition of EMC is, “What will the effect be on VMware hardware neutrality?” VMware typically supports; not just one server vendor, but all server vendors, not just EMC or Dell storage, but all storage, not just one networking vendor/Dell, but all networking vendors.

So what changes will Dell bring?

At the close of the Day 1 General Session Pat Gelsinger welcomed an unannounced visitor to the stage – Michael Dell. After a friendly chat, Dell answered (at least part of) the question people had been wondering.

Gelsinger: What impact will the Dell acquisition have on the VMware ecosystem?

Dell: “The Open Ecosystem of VMware is critical to success and won’t change” Only an ecosystem of this size and power could really pull off this cross-cloud vision…”

Will this hold true in the face of quarterly sales pressure? It is too early to tell….

-

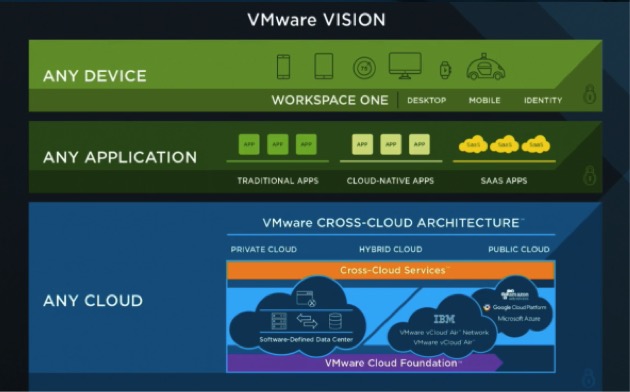

The VMware Vision remains the same – (with tweaks to nomenclature, additional pieces defined and new products)

VMware has been talking about a similar vision for several years. The biggest change this year at VMworld is flushing out of products to support this vision and the new focus on being able to manage any cloud under the “Cross-Cloud Architecture” (#1 on the list). Some of the products that support this vision are here today, and some are just taking shape. The End User Computing demo on day 2 gave a sense for the type of end user experience VMware is shooting for – but how close are customers to buying this (and how close is the complete solution?)

-

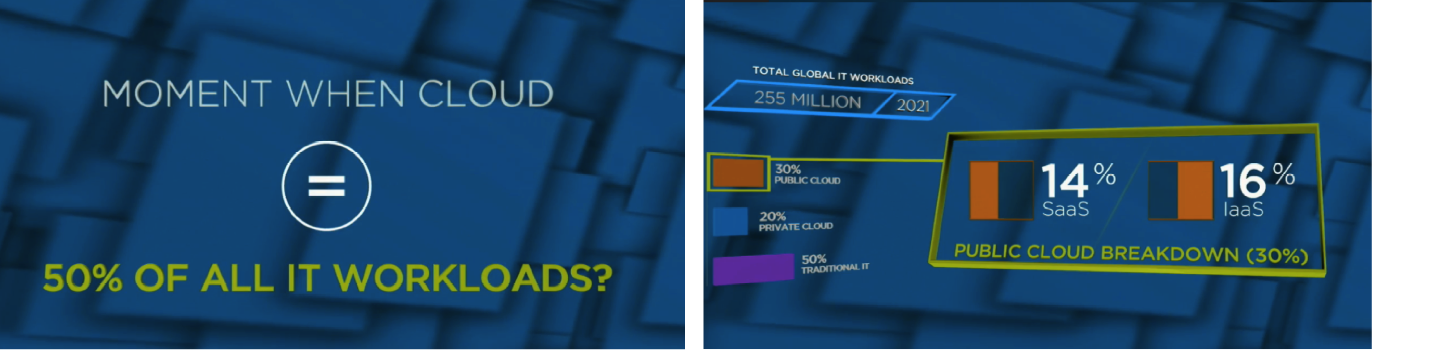

50% of apps on “cloud” in 2021? Interesting Metrics on Cloud Adoption today – and predictions for the Future

In his opening Keynote, VMware CEO Pat Gelsinger presented some interesting statistics compiled from analysts, public data and VMware data that provided a snapshot of where the “cloud” market has been – and what we may expect in the next 10+ years.

- 2006: 98% traditional IT, 2% Public Cloud (mostly salesforce.com)

- 2011: 87% traditional IT, 7% Public Cloud, 6% Private Cloud,

- 2016: 73% traditional IT, 15% Public Cloud 12% Private Cloud

- ** 2021: 50% traditional IT, 30% Public Cloud, 20% Private Cloud

- 2030: 19% traditional IT, 52% Public Cloud, 29% Private Cloud

What does all this mean and why did Gelsinger take such pains to share these numbers? In a market that big there will be “many clouds” – and VMware wants to be the one who extends their on-premise infrastructure to manage these clouds!

-

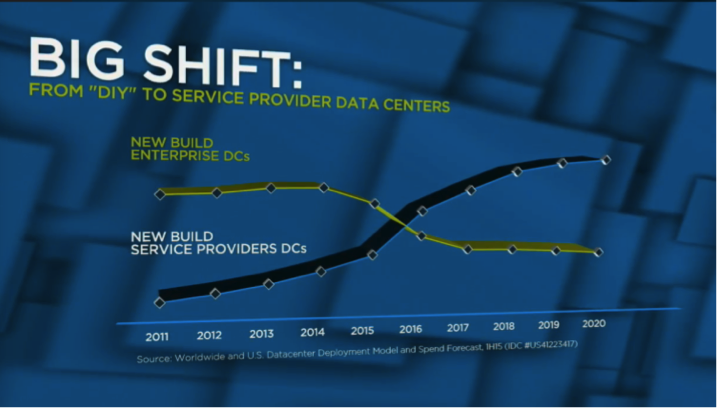

VMware increasing focus on $60B Opportunity with Service Providers

As customers move to cloud, service providers are buying more and more of the hardware and software required to run data centers. Gelsinger shared data that this 2016 is the year when the share of data center products purchased by service providers EQUALS the amount purchased by organizations for their IT.

VMware seems to be increasing focus on this opportunity. On the first day of the conference, VMware announced its partnership with IBM on Cross-Cloud Services, and the first opportunity he talked about in his session was what he called the the “Managed Cloud Services” (aka “Hosting”) Market. During the general session, he continually made reference to VMware’s large network of Service Provider partners, the vCloud Air Network.

-

“Hyper-converged Infrastructure, Powered by Virtual SAN”

In previous years, VMware has talked about converged and hyper-converged infrastructure in terms of EVO Rack and EVO Rail and their partnerships with hardware vendors, and talked about Virtual SAN as “storage product”. At VMworld 2016, the two messaging seemed to merge – Virtual SAN is both a storage product and a hyper-converged infrastructure product (Hey, it’s a desert topping AND a floor wax! – see the old SNL fake commercial).

Whatever you call it, VMware says Virtual SAN is “in the tornado” with 400% YtoY growth, 5,000 customers, and 100 new customers every week.

-

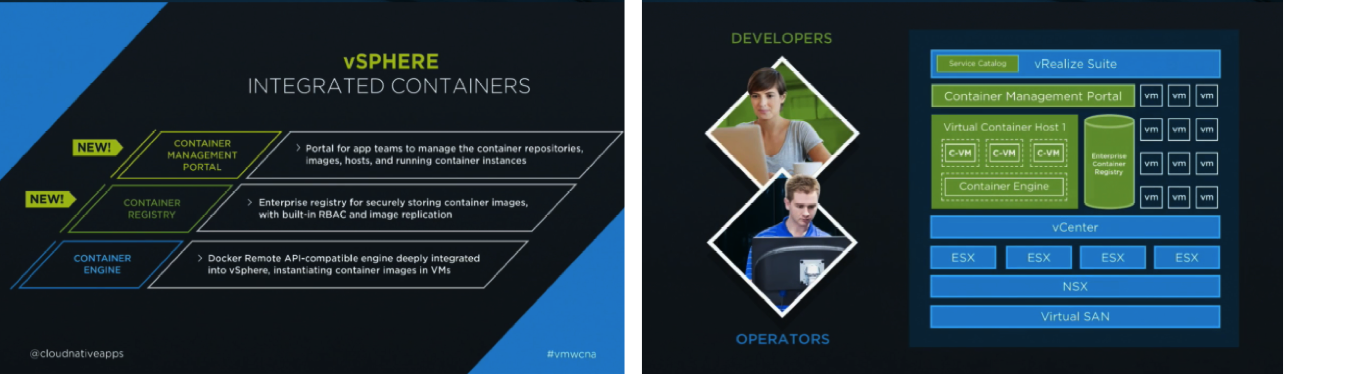

Bringing Containers into Virtual Infrastructure

vSphere Integrated Containers Working with the VMware SDDC Stack

During the Day 2 General Session, Kit Colbert, CTO for Cloud Native Apps provided an update on VMware’s approach for supporting the development of cloud native apps, and leveraging containers.

The majority of the session focused on updates to vSphere Integrated Containers including the new “Container Registry” and the new “Container Management Portal” and how the container approach leverages skills, tools and the virtual infrastructure companies already have, to provide security, management and availability to containers.

Kit also highlighted solutions that leverage the Photon platform the solution with Pivotal Cloud Foundry that was announced earlier this year and an offering with kubernetes that is coming soon.

Both VMware container product offerings are published as open source on GitHub

4. SDDC Products as the Building Block of Cross-Cloud Offering

While the both the Monday and Tuesday General Sessions had titles that included “cloud”, the star of the show is still VMware’s suite of products to deliver a software-defined data center (SDDC). If you look carefully at the vision for Hybrid Cloud, you see it is enabled by SDDC. When you look at the layers of VMware’s Vision – Any Device, Any Application, Any Cloud, you see that the building block is the SDDC.

vSphere is the foundation of this approach, but the focus on virtualized networking and security (with NSX) and software-defined storage (with Virtual SAN) with management and automation provided by vRealize. Each of these elements continue separately, but Day 2 demo focused on how everything fits together to give businesses the agility they need, while making life easier for developers and simpler for end users.

VMware has often made a lot of product announcements at VMworld, but this year has been different. Announcements have focused on broad new product offerings and in the Day 2 General Session, VMware CTO Ray O’Farrell told the audience to expect product updates to vSphere (and we assume the rest of SDDC) at VMworld Europe in October.

-

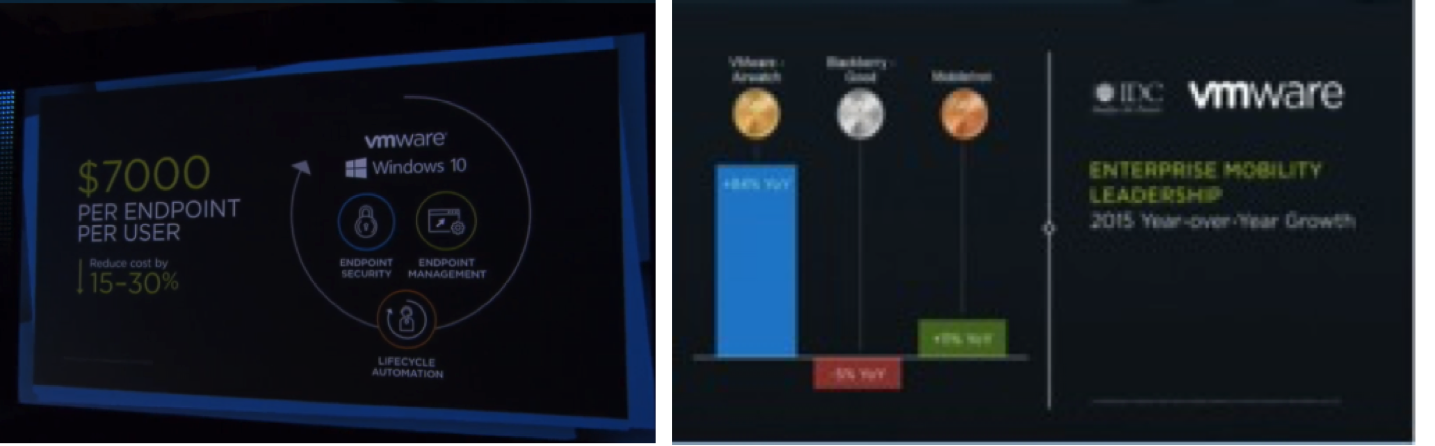

Maybe the time for Virtual Desktops and End User Computing is Finally Here?

Sanjay Poonen, VMware EVP of End User Computing kicked off the Day 2 General Session by focusing on the top section of the VMware Vision –

“Any Device” with End User Computing Products that include

- Apps and Identify

- Work across desktop and mobile and have

- Simple management and security built in everywhere

As discussed in previous VMworld’s, analysts and customers have shifted over the past few years to the point where VMware vision and execution are rated tops in magic quadrant and customer market share has shifted. In recent reports, VMware has reported that the End User Computing business is now a $1.2Billion business. Part of that is driven by enabling 15-30% lower costs per user driven by improvements in the products and part is attributable to the increasingly robust solution – particularly the AirWatch platform for mobile management.

Most of the session was an impressive demo that showed the capabilities of the platform to provide a simple and powerful end user experience to deliver all of a users applications through Apple devices, Android devices and Windows 10 desktops and leverage the built in identify management, security and availability of the platform.

-

Security (and NSX) is everywhere – in every topic, in every demo and with every customer testimonial

Security was not a stand-alone topic in the General Session and perhaps this is a sign of its increasing importance and improvements in the VMware products? Instead, security and compliance were a part of the discussion during every topic of the general session.

| · Cross-Cloud Architecture

· NSX as part of SDDC platform · Visibility with vRealize Operations · Security moving with workloads – from vRealize Automation · Micro-segmentation as a core capability of NSX |

· Encryption built into security policies and enabled by NSX

· Security built into into SDDC, supporting Hybrid Cloud and Cross-Cloud Architecture · Security built into Horizon, AirWatch and End User Computing |

and the #1 Takeway from VMworld is

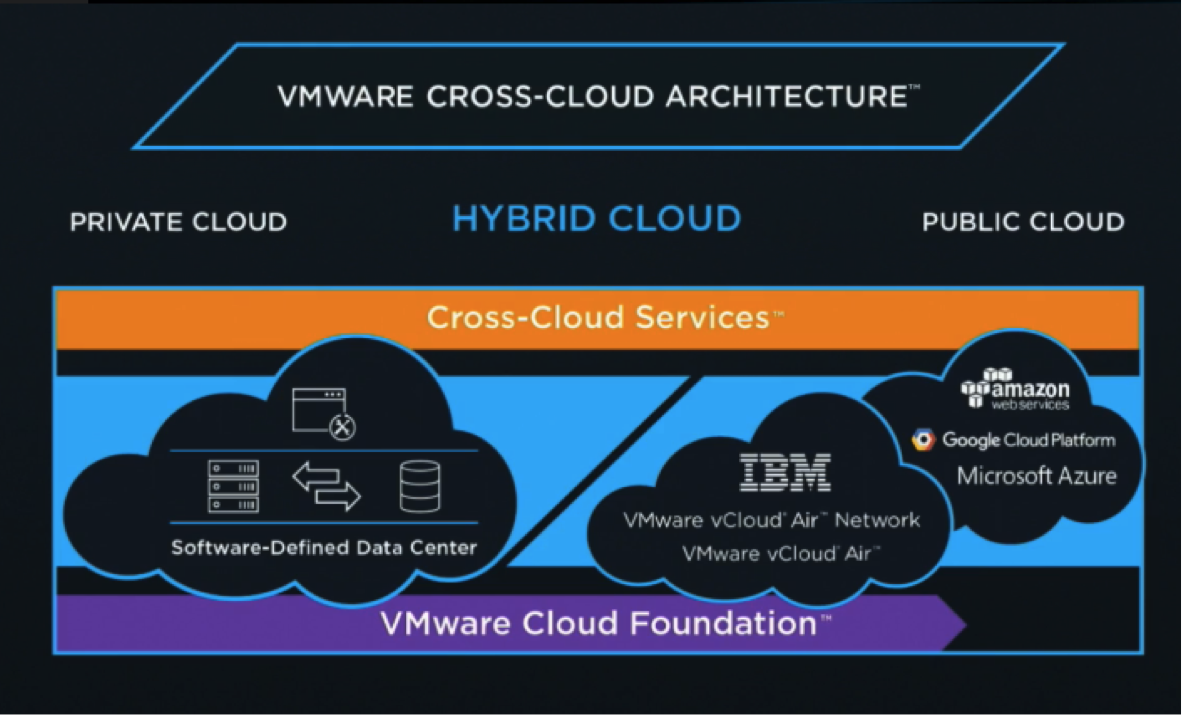

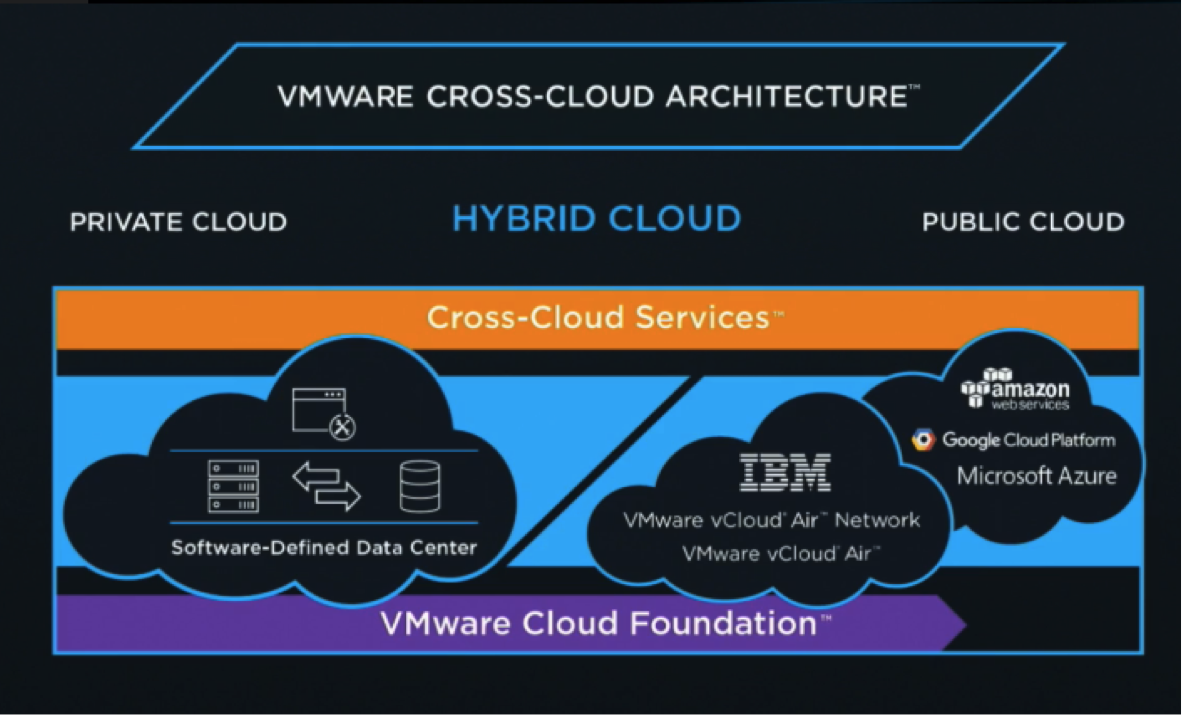

Cross-Cloud Architecture (including VMware Cloud Foundation and Cross-Cloud Services

All of the traditional hardware and software IT vendors have been struggling for a few years to determine what their role was in “cloud”. Some bought service providers, some built services, some tried to “SaaSify” their applications.

VMware has been on a dual approach of 1) building their own cloud service with vCloud Air and 2) selling their products as infrastructure components to Service Providers to build their own cloud offerings.

With vCloud Air receiving very little attention in general sessions and the focus on partnerships, it appears VMware seems to have pivoted on their “cloud” strategy to:

- Offer a compatibility layer between the megaclouds (AWS, Azure and IBM) that ties to their virtual infrastructure

- Continued/Increased focus on selling their technology stack into Service Providers.

They call this compatibility layer, “The VMware Cross-Cloud Architecture” and the 2 main components are a) new product called VMware Cloud Foundation which provides a unified SDDC platform for the Hybrid Cloud and 2) a set of Cross-Cloud Services that provide security, availability and agility – and tie to the core SDDC infrastructure. Is this really a new product or just a re-packaging of VMware’s cloud portfolio? You can decide for yourself by looking at the CTO blog (see link below) and visiting the tech previews at the VMworld hands-on-labs.

As part of this focus, VMware announced a partnership with IBM, and plans to partner broadly to this architecture as an abstraction layer across clouds.

Want more information? Follow the links below to articles, blog posts etc…

- Click here to see the recorded Monday General Session replay

- “Competitive Advantage in the Multi-Cloud Era

Connecting People, Apps & Data to Propel your Business Forward

- “Competitive Advantage in the Multi-Cloud Era

- Click here for replay of Tuesday General session:

- Competitive Advantage in the Multi-Cloud Era

Connecting People, Apps & Data to Propel your Business Forward

- Competitive Advantage in the Multi-Cloud Era

- VMware CTO Blog post on VMware Cloud Foundation

- “VMware Cloud Foundation, the Unified SDDC Platform for the Hybrid Cloud is Here!”

- * Includes list of Hands On Labs

- Top “Cross-Cloud Management Sessions at VMworld 2016

- ZDnet article: VMware’s Next Play: Managing all clouds for enterprises

- VMworld “Highlights” website

- VMworld Social Media stream

- Product Announcements at a Glance

- Press Releases

- VMware Unveils Cross Cloud Architecture VMware Cloud Foundation(TM) Makes It Easy to Manage and Run SDDC Clouds; New Cross-Cloud Services(TM) Will Enable Customers to Manage, Govern, and Secure Applications Running Across Public Clouds, Including AWS, Azure and IBM Cloud

- VMware Delivers Innovations to the Digital Workspace With Unified Endpoint Management, Windows 10 Support and Enhanced Identity Management

- VMware Extends Capabilities of vSphere Integrated Containers to Help Enterprises Embrace Digital Business

- VMware Further Simplifies Production Deployment of OpenStack Clouds With VMware Integrated OpenStack 3

I welcome any comments below — And make sure you “Follow” our blog (look for the “Follow” link on the left sidebar) and have your say. I’m also available as a public speaker, to support local and global events in Silicon Valley, or the rest of the flattening world…

For more details, and to stay in touch with this community, contact me or Subscribe to our “Climbing Out of the Box” Newsletter via the form below.

Is Your “Partial-Channel” Business Stalling? 3 Human Emotions that Prevent Traction

Recently I had a call with a channel director for a company based in India. His company sold software for banks and he managed their channel for them across the Asia-Pacific. region. It struck me that the challenges they faced is common to many companies in the tech industry – and beyond, and that they were rooted in decisions made years ago by his company, when they set their route-to-market strategy.

His company had sold “direct” until about 5 years ago when they started adding “some channel”. Now they had a loose network of 1-2 companies per country who acted as “Agents” for them in Australia, Singapore, Taiwan, Malaysia, Vietnam, Thailand, etc.… He had previously managed their business in Europe and they had the same setup – and the same challenges….

Of the 20 or so countries he managed, with nearly 50 partners, he only considered 3-5 partners to be focused and enabled on his business. His plan was to get another 3-5 enabled in 2016. He’d done this before and knew he would need to 1) focus on a country or set of partners, ) he would need to spend a lot of time with the partners’ technical team to help them get “enabled” and 3) he would need to get them engaged with his field sales team with account targeting. But since he had gone through this process before, he also knew just how hard this was going to be – and in the end, that it was a gamble that might not work…

What Could the Channel Rep/the Company do to Become Relevant to Partners and Gain Their Focus and Commitment?

The company had a sales rep or two in each of these countries, and as we discussed the situation, what jumped out at me was the shallow relationship that the vendor seemed to have with these Partners. Sometimes they would be engaged (when the vendor brought them into a deal), but then they would not talk for a few months. In the channel manager’s heart, he knew that every week that went by without engaging, meant the Partners’ business was moving farther away from selling his product…

So what was the “Route-to-Market” decision that led to these issues?

The decision to have a “Partial-Channel” Sales Model!

What I mean by “partial channel” sales model is that some business is sold by partners, and they get compensated for what they sell, but a lot of the business is sold directly by vendor sales reps without involvement or compensation for any partner. They have “some partners”, but neither party is very committed to the relationship.

My experience is that

- Vendors can have some success selling “Direct” (particularly in specific segments/markets)

OR

- They can be successful with an “Indirect” (or channel) sales model.

But it is hard to be successful with “partial-channel” sales model.

The results are like the old saying, “You cannot be ½ pregnant”. Either you work with partners, or you do not. Working with partners only when it is “convenient” does not result in a true partnership (or much revenue).

So why is this the case? A “partial-channel”sales model makes building a channel difficult because it runs completely against 3 Powerful Human Emotions that dictate both vendor and partner behavior. These 3 emotions are incredibly powerful and stack the deck against a “middle-path” on channel –

- Trust

- Envy

- Greed

Let’s discuss each of these emotions and the dynamics of selling in a bit more detail.

Trust

We intuitively understand that “Trust” is a good thing in a partnership – but clearly lack of trust can have a very bad impact. Unfortunately, a “partial-channel” model tends to create a lack of trust between a vendor and their partners.

Think of it this way – on Monday, you make a sales call together, with your partner. But what is the vendor sales rep doing the rest of the week? In a “partial-channel” model, the answer often is, “calling on customers direct”. That’s OK and was probably the situation when the partner signed on, but it makes the partner ask themselves questions like:

- “Why didn’t the vendor ask me to work with them on ABC opportunity (that I heard about in an RFP)?”

- They sold XYZ opportunity direct – and I’ve known that account for years…

- I just invested in training on their new product, how could I recover my costs if they don’t work with me?

- I wonder how they decide when to work with me? It is probably just their sales rep trying to make more money on the deal by keeping me out…

All of these questions indicate a lack of trust in the partnership – and make it less likely a partner will commit, invest and initiate new sales opportunity for your products…

Envy

Google dictionary defines envy as “a feeling of discontentment or resentful longing aroused by someone else’s possessions, qualities or luck.” When a vendor has a “partial-channel” sales model, they often create guidelines for when they will sell “direct”. For example, they might say they will sell direct only to a) some named accounts, b) their current customers, c) some particular geographic area or d) specific vertical markets (such as financial services).

The problem with these carve-outs is that they create “envy” in the channel. Even if the reasons for the approach make sense on the surface, they create a dynamic of “envy” where a Partner tends to ask themselves questions like:

- “What if I did invest more in selling Vendor A,’s products? I can only sell it to some of my customers. I’m limited, and they are keeping the best accounts for themselves.

- “I wonder if there is even any opportunity in the accounts/markets where I can sell? It might be a waste of my time – and then they may take other customers/segments direct later (lack of trust) ?”

- Why bother – I have better opportunities to pursue…”

Greed

The last emotion that keeps a “partial-partner” sales model from thriving is “Greed”. Once again, some business is “Direct” and some business is “Partner”. The question becomes “How” does the vendor decide what is “Direct” and more importantly “Who” decides. The reality is that in many organizations, the field rep is loosely managed and can make the call whether to leverage partners or not. At some level that makes 100% sense – since they are in the best position to judge the customer situation and the partner capabilities to support the deal.

Unfortunately that is where “Greed” comes in. I cannot count the number of stories I have heard over the years from partners, from channel sales managers and even from sales reps, recounting that the deciding factor in whether to use partners was “How much will I get paid on this deal?”.

Many vendor compensation plans pay less to a rep on deals that go through the channel – because they get paid on the net selling price (which is the price paid by the customer minus discounts taken distribution/ resellers). In the short term, the Rep gets paid more if they sell direct. In the long term, he may/may not realize/or believe that he would get paid more if they had a strong channel in their patch. But the lure of higher compensation today makes the long-term question disappear for many reps and for many vendors…

So What are the options if you are stuck in the middle with a “Partial-Channel? Sales model?

In my experience, if a vendor has decided they need a channel, then they need to go “all in” and be willing to have a business that is 100% “channel touch”. They can still set up programs to differentiate channel margins or commissions based on role the partner played, but the assumption needs to be the partner is involved at some level in every deal. With this mandate, the vendor field reps are encouraged to use “team selling” and know they cannot sell around the partners, just to maximize the value of a first deal. That policy provides some incentive to support and enable partners. At the very least, partners are involved in fulfillment – which helps some with “Envy” and “Greed”.

It takes a lot more than that to create a strong partnership – and to begin to build “Trust”. The goal is to get partners to go beyond reactive to proactively creating sales opportunities. A lot of things need to change in the vendor’s GTM to make this happen (strong channel program with incentives, field engagement model, partner enablement, etc.…). But the first step is knocking down (or at least minimizing) Envy and Greed that having a direct team “in competition” with the channel creates. It is not the end of your journey to driving more channel revenue, but at least it is a start…

I welcome any comments below — And make sure you “Follow” our blog (look for the “Follow” link on the left sidebar) and have your say. I’m also available as a public speaker, to support local and global events in Silicon Valley, or the rest of the flattening world…

For more details, and to stay in touch with this community, contact me or Subscribe to our “Climbing Out of the Box” Newsletter via the form below.

3 Favorite Books that Illuminate the “Soul of Modern China”

In recent months, my thoughts have often been pulled from the world of technology, to the larger WORLD – as defined by geopolitical, cultural and economic conflict and all-too-often WAR. My deepest fears stem from the re-emergence of a militaristic Russia, with unrest and war in the Ukraine and the elsewhere in former-soviet Republics – and Russia’s increasing military involvement in Syria and the Middle East.

But I cannot help thinking that a US-centric perspective that dates back to Cold War stereotypes of a “good” US and Western Europe vs. an “evil empire” USSR/Russia misses what is really happening in the world. One of the obvious omissions of this world-view is that it discounts the impact of the rest of the world, and in particular, the economic re-emergence and the increasing political influence of China.

China has been, and is an economic juggernaut, finally progressing forward, as the government has let go of the some of the artificial controls and tries to move to a balance of Communism government and Capitalist economic policy. In the past couple of weeks, there has been some big news on China’s population and demographics problems that remind us of social and economic challenges to come.

- The October 29th official end of China’s “one-child policy”, adopted in 1978, which led to worker shortages and a large imbalance between the number of males and females…

- A recent article I read in the Economist shocked me to the core. Chinese policies intending to discourage moving to the cities for work have instead led to “106m children’s lives were being profoundly disrupted (many of them left behind in the care of grandparents, or no one in particular) by their parents’ restless search for jobs. For comparison, the total number of children in the United States is 73 million. Very had to imagine…

I have always been interested in China, partly because of the exotic images of ancient China, with elaborate temples and palaces, wise-looking emperors with “Manchu” mustaches, and the image of the Great Wall of China standing as a barrier to the Mongol hordes.

But the other part of my interest is personal.

- My grandmother was born in Shanghai in 1904, one of 5 children of an American teaching in a Chinese University at the turn of the century. She went on to write more than 50 children’s books under her maiden name, Eleanor Frances Lattimore, quite a number of them about children in early 20th century China.

- I was also interested in the story of my great-uncle, her brother, Owen Lattimore, who became a leading China expert, and was an emissary from President Franklin Roosevelt to Chiang Kai-Shek. He was a scapegoat of anti-communist fear from “McCarthyism”, and when China was “lost” to the Communists under Mao, he was falsely accused of being “a top soviet spy”.

Over the years I have ready many books about China, but below are the three books that I find myself recommending over and over to friends. I found each of these books both interesting and entertaining in their own way and together, they seem to provide a good tutorial for a “westerner” seeking to gain insight into the mysteries of modern china.

3 Favorite Books that Illuminate the “Soul of Modern China”

I may be a bit biased on the first book, but Little Pear was my grandmother’s first and most popular book and it helped me see China and Chinese people as just like everyone else (but more exotic?). It published in 1930, was available in more than 30 languages and is still in print today. One of the reviews on Amazon.com summarizes the universal appeal well.

“Little Pear is an endearing (and enduring) character, and the stories are sweet and uncomplicated. Despite his being from another time and another place, children can easily identify with the title character, his feelings, and his adventures.”

The summary on Amazon.com does a great job of summarizing why this non-fiction book is so compelling and illuminating.

“Jung Chang describes the extraordinary lives and experiences of her family members: her grandmother, a warlord’s concubine; her mother’s struggles as a young idealistic Communist; and her parents’ experience as members of the Communist elite and their ordeal during the Cultural Revolution.

Chang was a Red Guard briefly at the age of fourteen, then worked as a peasant, a “barefoot doctor,” a steelworker, and an electrician. As the story of each generation unfolds, Chang captures in gripping, moving—and ultimately uplifting—detail the cycles of violent drama visited on her own family and millions of others caught in the whirlwind of history.”

I read this book in 2014, in part because I wanted to understand the world of China before Communist China and the disastrous “Cultural Revolution” that was my first awareness of China as a teenager. I was also intrigued by Madame Chaing’s role in history – a Chinese woman who went to college in the US and rose to be one of the most famous and influential people in the world during the Cold War era.

“…Madame Chiang Kai-Shek is at the center of one of the great dramas of the twentieth century. This is the story of the founding of modern China, starting with a revolution that swept away more than 2,000 years of monarchy, followed by World War II, and ending in eventual loss to the Communists and exile in Taipei.”

The book delivered much more than I expected, providing new insights into the history of China, its people, and the complete separation of the ruling Chinese class from the problems and interests of their people. Stories of backroom deals with “warlords” that controlled vast sections of a fragmented China and scandalous corruption read like fiction – until you realize that how deeply corruption has been woven into the fabric of Chinese politics throughout history.

Additional Recommendation

“Mao: The Unknown Story”, is a riveting book by Jung Chang, the same author as Wild Swans above. It is a scathing biography that provides a portrait of Mao as one of the truly evil, destructive men in history – with hundreds of interviews with childhood friends, former family servants, party members, opponents and others that provide evidence to support this appalling picture….

I welcome any comments below — And make sure you “Follow” our blog (look for the “Follow” link on the left sidebar) and have your say. I’m also available as a public speaker, to support local and global events in Silicon Valley, or the rest of the flattening world…

2015 VMworld Top 10 List: What’s the Buzz?

Lots of information from VMworld 2015 and as usual the show floor was the place to check out the reality behind the PowerPoint slides… VMware has done a better job than most tech vendors at delivering innovation and products that really help customers. Let’s check out the Top 10 things from VMworld first 2 days.

- Cloud Academy and the “Squeaking Apps”

VMware used this surreal headmaster to introduce the curriculum at the Cloud Academy and the One Cloud, Any Application, Any Device mantra. But the guy with the cloud head was scary and when the squeaking apps attacked VMware President, Carl Eschenbach, you sensed that he really did want to kick one of the little guys…

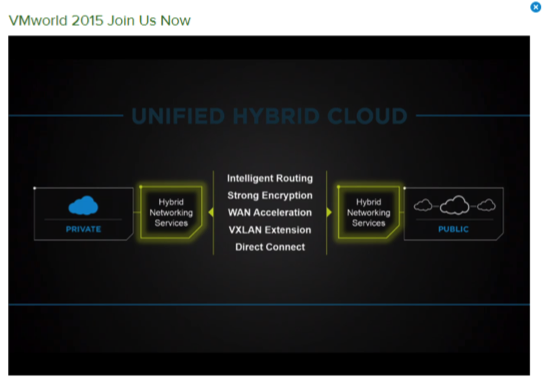

- Applications are becoming Hybrid, Driving the Need for the Unified Hybrid Cloud

VMware has been talking about “Hybrid Cloud” for a while, but at VMworld 2015 it become “Unified”. The change to me was the focus on applications. Why do you need a “Hybrid Cloud”? Because we all know that applications are becoming Hybrid for cloud native apps, as enterprises seek to use SaaS versions of their applications and as multi-tier apps become have cloud and on-premise components…

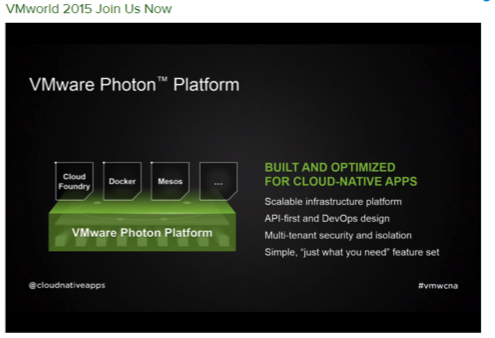

- Two VMware Options to Leverage Containers: vSphere Integrated Containers and VMware Photon Platform

VMware spent a lot of time talking about their approach for cloud native applications and at VMworld they put some meat and products behind the story.

- For customers who want to use containers within their infrastructure, VMware announced VMware vSphere Integrated Containers, to allow a VMware environment to recognize the characteristics of the container and the VM.

- For customers developing CNAs from scratch, they announced that “they would create a new platform. The approach builds on “project photon” announced in Feb 2015, and becomes VMware Photon Platform.

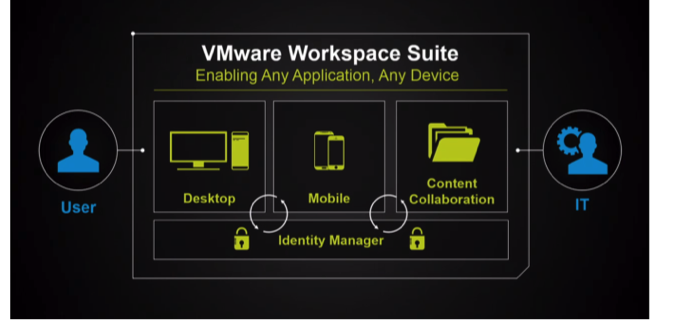

- VMware Workspace Suite Takes Shape

For a couple of years, VMware has been talking about End User Computing in terms of “how end users access applications on multiple devices”, which encompassed mobility. At VMworld the products behind this vision became much more clear with SDDC as the underlying infrastructure, Desktop VDI consisting of traditional VDI, Mobility Management as defined by AirWatch as the second pillar, and new content collaboration tools as the third pillar of the VMware Workspace Suite

- Best Quote of the Keynote – from a Customer!

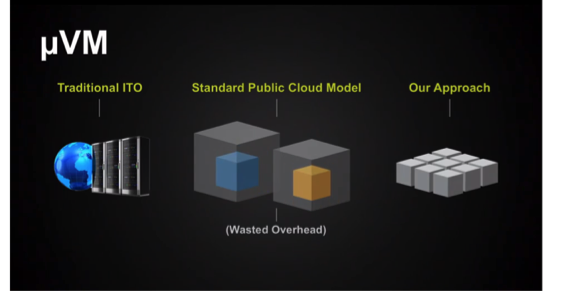

- Virtustream for Managed Unified Hybrid Cloud

Virtustream is now a Federation company, joining EMC, VMware, Pivotal, RSA and VCE. CEO Rodney Rogers outlined the value proposition for managed services above the virtualization layer. By aggregating unused infrastructure capacity into what Rogers called micro-VMs, Virtustream can drive tremendous improvements in resource utilization – and save lots of money on hardware…

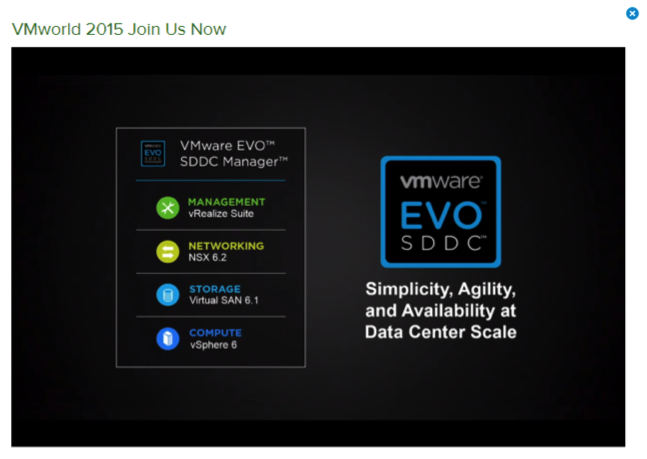

- EVO Rack Becomes EVO SDDC / EVO SDDC Manager

More name changing from VMware, but the change makes sense to me… While this integrated, converged infrastructure + SDDC platform has been for some time with versions from suppliers like EMC, the full “Rack” version including VMware NSX and management has not been announced. EVO SDDC seems to come in 2 versions – one with the converged hardware and the full SDDC, and one that has the SDDC portion that enables you to manage an existing hardware stack.

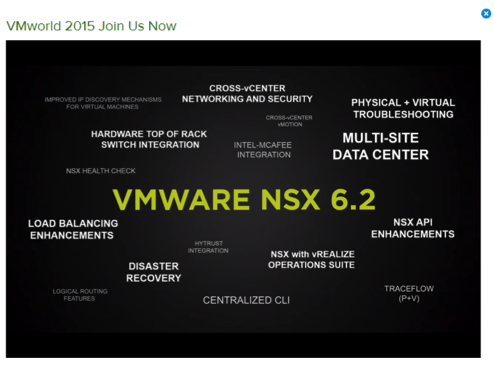

- NSX is a Game Changer – Architect Security into the SDDC

NSX has been around for 2 years and VMware talked about customer momentum that was “horizontal” (not limited to a few verticals or really big companies). The Network was positioned as the underlying fabric needed for a unified hybrid cloud – but security is a gap today that the micro-segmentation of NSX uniquely solves.

- Hybrid Networking is the “tough problem”: Solved by NSX in for the Unified Hybrid Cloud

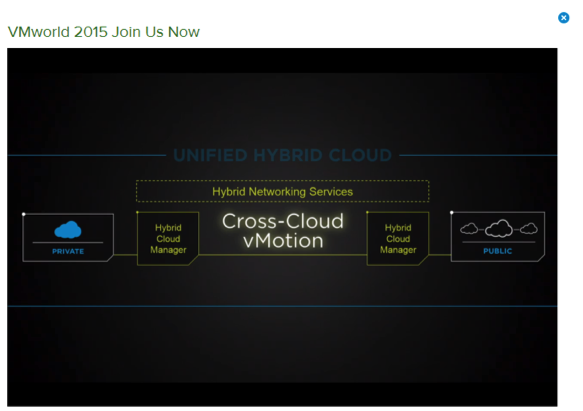

Organizations cannot get to the agility they need with the current network bottleneck. By providing a virtualized layer customers are finding that NSX gives them the network services they need across boundaries – including cross-cloud vMotion!

And the #1 VMworld Moment is “Cross-Cloud vMotion”

In the Monday General Session, VMware CTO Ray O’Farrell and VP of Engineering Yangbing Li demonstrated this capability, which I believe they said as in “Tech Preview” at VMworld. The industry has been looking for long distance for a while and demo of cross-cloud seemed pretty darn exciting to the audience…

I welcome any comments below — And make sure you “Follow” our blog (look for the “Follow” link on the left sidebar) and have your say. I’m also available as a public speaker, to support local and global events in Silicon Valley, or the rest of the flattening world…

For more details, and to stay in touch with this community, contact me or Subscribe to our “Climbing Out of the Box” Newsletter via the form below.

Contact form

(Shared) Sales Force Not Selling (all of) Your Products? Three Common Levers to Create Sales Focus (Part 3 of Series)

In the first post of this series, I discussed the widespread assumption in the Tech industry that shared sales forces help encourage “Survival of the Fittest” products. In the second part of the series, I discussed a checklist you can use to determine if your products can be sold via a shared sales force.

In today’s post, I will be talking about the Pros, Cons and Reality of the “Three Common Levers to Create Sales Team Focus”

Does “Survival of the Fittest” work for a shared sales force? Sometimes, but from what I’ve seen, more often there are major distortions to the “fittest” based on other factors that drive attractiveness to sales. In my experience the products that get sold by a shared sales force are not necessarily “the fittest”, but instead, the products that meet more “human” needs – like reps looking to meet their quota, hit their “accelerators”, or even just to keep their jobs for next quarter – and are often dictated by the comp plan. The way they vote with their time may or may not coincide with what the executives feel are the longer term interests of the company. Of course, a company falters if they miss short term performance needs, but I would argue that just as many tech companies falter when they sell the “products they know, or can sell fastest, until the differentiation for those products withers and they and the company are left in a weak strategic position…

In my experience, there are 3 main tools that most tech organizations use to gain sales rep focus.

3 Tools to Manage “Product Sales” in a Shared Sales Force

- Tool #1: Provide Transactional Incentives for Product Sales

- Tool #2: Provide Sales Overlays to Create Additional Sales Focus and Expertise

- Tool #3: Adjust the Compensation Plan to Provide Incentive to Sell Products

Tool #1: Provide Transactional Incentives for Product Sales

Creating Focus

Transactional incentives are the most common approach to influence sales rep behavior and focus. We’ve all seen this approach till we are numb and a bit confused by the overlapping incentives that are running from different groups each quarter.

Pros

- $s influence a coin-operated sales team

- Can be effective for transactional sales

Cons

Is “lack of an incentive” really the reason you don’t have focus on all your products?

- More often the issue is lack of sales fit see the Shared Sales Force Checklist

- Is the amount and type of incentive really enough to change behavior? If your rep is selling $ million deals is $1,500 going to change behavior?

- Also check out my post, “Channel Not Selling Your Products? 3 Questions You Can Ask to Diagnose the Problem” (much of this post applies to your reps too)

Tool #2: Provide Sales Overlays to Create Additional Sales Focus and Expertise

Creating Focus

Since Overlays only sell particular products, they can’t get distracted by easier sales, and they wake up every morning trying to sell your product. Often these overlays are SEs, so they can provide both technical expertise and some sales coaching specific to the product.

Pros

- Have a team focused on successful selling of a product

- Provide a feedback loop for product marketing or business units seeking customer feedback on their market

Cons

- Typically provide double compensation for the same sale, to encourage collaboration

- And as any sales executive knows, you don’t want to pay 120% of sales payout for 80% achievement…

- Sales overlays have different goals and it is common for organizations to have INTERNAL sales engagement across products. As companies get larger (think HP, Cisco, even mid-sized companies like VMware) different Reps have different agendas at the same customer

- The Account Reps/Teams who own the overall account and get credit for all sales into the account

- A great vendor sales rep is often quite “controlling” of the decision makers and timing for discussions within their accounts, and this instinct tends to undermine efforts by those who have different roles, including:

- Your Sales Overlay Teams that must sell their product

- Your Strategic Alliances that are trying to sell joint solutions into the same account

- Your Channel partners who might be selling your product as part of a larger solution that won’t close till next quarter

Tool #3: Adjust the Compensation Plan to Provide Incentive to Sell Products

The most common approach to setting a compensation plan is “a dollar is a dollar”, where the comp plan does not differentiate whether the sale is for Product A, Product B, Training or Professional Services ($ all goes to the same place anyway, right…???)

Creating Focus

- Quota for individual product groups. For example, a Reps $500K quarterly target might include a minimum $100K from a particular “Strategic” product group

- Accelerators for certain “emerging/strategic” products (e.g. earn 150% quota credit for selling emerging Product X)

- Carve-outs – making some easier, “low-hanging fruit products” or categories of sales not part of the compensation plan. For example, many/most technology vendors do not pay their field account reps for Renewals, because that might unnaturally incent Reps to “farm” the renewals business, rather than “hunt” for new business

Pros

- $s influence a coin-operated sales team

- Impact to compensation can be significant enough to influence behavior (more than incentives)

Cons

- Must be utilized sparingly, or comp plan is too complex and Reps get mixed signals on organization priorities

- Complex comp plan with accelerated payout can result in sales reps making their number, but the organization missing bookings, revenue and profit forecasts.

But here is the dirty little secret of shared sales forces…

Even if you can assign a Product-Specific quota and have an Overlay Sales Force it is quite possible that your organization will lose sales focus (and revenue) on some products

What can organizations do to have a cost effective sales force and sell all their products? In next weeks post I will talk about some “Out of the Box” approaches organizations can use to gain the cost advantages of Shared Sales Forces AND Sell a wide range of products.

I welcome any comments below — And make sure you “Follow” our blog (look for the “Follow” link on the left sidebar) and have your say. I’m also available as a public speaker, to support local and global events in Silicon Valley, or the rest of the flattening world…

For more details, and to stay in touch with this community, contact me or Subscribe to our “Climbing Out of the Box” Newsletter via the form below.

(Shared) Sales Force Not Selling (all of) Your Products? Use the “Shared Salesforce Checklist” to Uncover the Issue (Part 2 of Series)

Last week I talked about challenges tech organizations encounter when they use a shared sales force to sell multiple product groups. The organization may indeed recognize increased sales efficiency, but also may see a drop in sales and profits derived from some products. Which of these effects is larger depends on your business – but beware of adopting a shared sales force, without taking a hard look at the potential negative impacts on some parts of your business.

(Shared) Sales Force Not Selling (all of) Your Products?

In Part 2 of the series, we will talk about the variables that make a shared sales force across products a success, and when the benefits are an illusion.

When does using a shared sales force work well?

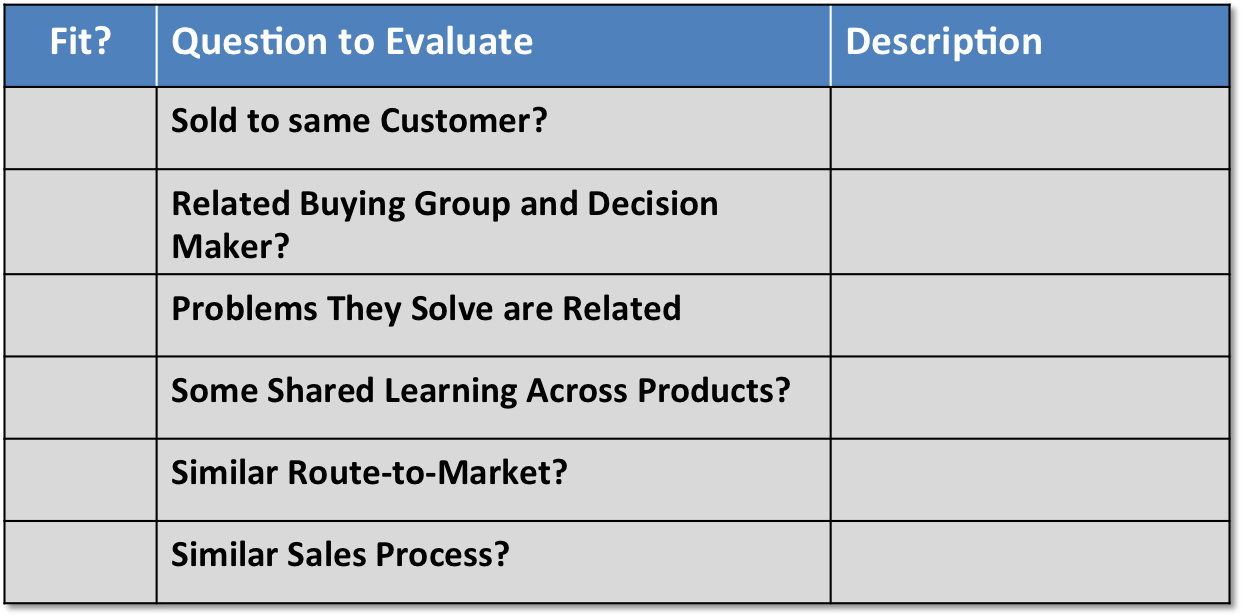

At a high level, it can work well when the products or the business model for the products being sold fit together in some way. In this weeks’ post I will explore this fit in more detail and talk about a tool that I have developed and have used over the years to help companies think through when a shared sales force approach makes sense for an organization. I call this tool, “The Shared Sales Force Checklist”, and the checklist is shown in Figure 1 below.

A good way to get started is to complete the checklist yourself, and then get additional perspectives from customers, and folks within your sales, marketing and product organizations. You will notice that while the questions are Yes/No, you need to think about the underlying question before you decide if the answer is the same for both products. For example, to answer, “Sold to Same Customer”, you need to define target customer for each product. You can use the “Description” column on the right to fill in these details. By comparing the answers from customers and your internal staff, you can make a lot of progress determining how well your products fit together for a shared sales force.

Figure 1: The “Shared Sales Force Checklist”

Let’s take a look at the questions in the Checklist in more detail. A single shared sales force selling multiple product groups can work well when:

- They are Targeted to the Same Organization

- If you are selling to different types of organizations, you may not be able to get sufficient customer intimacy to sell both product groups For example, problems can arise if one product is sold mainly to Healthcare and another is sold as a horizontal sale across industries.

- They are Sold to the Same Buying Group and Decision-Makers

- If you must sell to very different buying groups within an organization – like Line of Business for one product and IT Operations team for another, you may find that it requires a completely separate set of sales calls and account relationships.

- They Solve Related Problems and are Part of Complementary Solutions

- If two products are part of the same solution, like two components of the corporate network, you may find that both projects are part of some of the same projects – and therefore get solution synergy.

- There is “Shared Learning” Across Products

- If two product groups have a different set of baseline technology and industry learning needed to sell them effectively, training can be difficult and the sales team may resist requirements for hours of enablement training.

- For example, it may be difficult to sell one product that fits into the network and another product that optimizes storage with one sales force. Your sales team would need to be educated on technology, industry trends, problems and competitors for two separate ecosystems of vendors – a lot to ask for a group of employees who are supposed to be spending their time with customers…

There are also some other significant elements of the GTM for Products that can accelerate or sabotage efforts to share a sales force, and in my experience, organizations tend to overlook or discount their importance. A single shared sales force selling multiple product groups can work well when:

- They Have a Similar Sales Process

- For example, if one product is sold transactionally based on price, and another is a consultative ROI-based sale, they will be very hard to sell with one sales force.

- I saw this in one client where they had two similar products, but one was sold directly to developer teams and the other was an Enterprise sale. The Product Marketing folks that sold to developers kept expecting the sales team to carve out part of their time to sell their product, but were consistently disappointed…

- They Have a Similar Route-to-Market

- For example, if one product is sold by a group of Enterprise Sales Reps on Global Accounts and another is sold by System Integrators who build the product into their solutions, they will be hard to sell with one sales force

In next week’s post, I will talk about the 3 main tools that Technology vendors use to prevent issues with using a shared using force, when these tools are effective (and when they don’t have the intended consequences…)

I welcome any comments below — And make sure you “Follow” our blog (look for the “Follow” link on the upper left) and have your say. I’m also available as a public speaker, to support local and global events in Silicon Valley, or the rest of the flattening world…

(Shared) Sales Force Not Selling (all of) Your Products? (Part 1 of a Series)

For many technology vendors, a Shared Sales Force across multiple product groups is reality of how they go to market and sell their products. Sometimes this approach brings the hoped-for coverage synergy and robust bookings, But as we have all seen in our careers, sometimes “things don’t work out so well…” If you’ve had the role of VP/GM or Product Marketing for a product business unit, you know that

“SHARED SALES FORCE” OFTEN EQUALS BUSINESS UNIT FRUSTRATION AND LOW SALES $

A friend of mine used to be the VP and GM of a Product Business Unit with a tech vendor with many product groups and about $700M in revenue. His organization used a shared sales force across many business units, and his business was allocated a share of the cost of several other sales organizations within the company (that could conceivably sell his products). The problem was that despite all of these “allocated” sales resources, none of the sales teams to spent time selling his product (which did not help his BU performance…). After a year or so, he concluded that he could not control his own destiny, and he chose to move on to greener pastures.

The challenge is that when organizations use a shared sales force across multiple product groups, the sales team is asked to vote with their time, by focusing on selling some products and not others. The Tech industry generally sees this decision as an application of Darwin’s “Survival of the Fittest” theories on evolution, to “Survival of the Fittest” tech products.

Shared Sales Forces are usually seen as a way to gain sales efficiency. While it always makes sense to look for ways to reduce the cost of sales…

My experience is that tech vendors often make the decision to use a “Shared Sales Force” without fully accounting for how the approach will also reduce revenue (and profit) for some products…

Some lost revenue is inevitable and planned for, but what if some of the product groups lose a significant amount of their sales, or even just do not grow as expected. Would the decision to use a shared sales force still make sense? Of course the answer is “it depends”, but I think it is fairly common practice is to make the change to a shared sales force based on “financial necessity”, and assume that the BUs and the Sales Team will “figure out a way to make it work”.

The issue is that what often what happens is an accompanying reduction in sales and profit from some products – which can make a decision made for a “financial necessity” into a “financial disaster”…

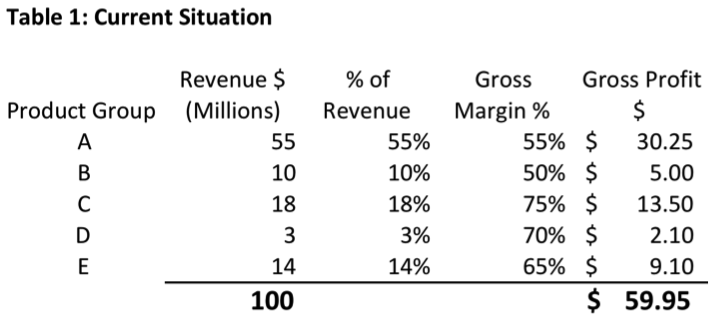

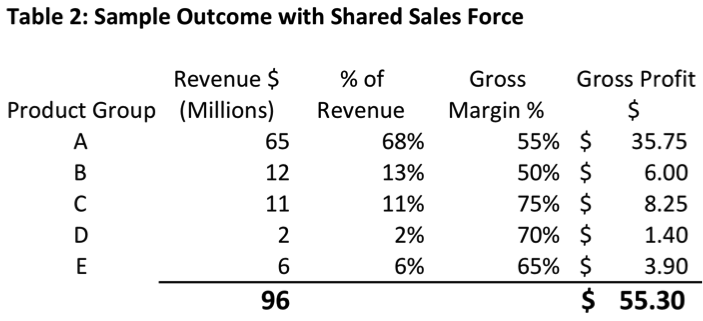

Let’s take a look at a sample scenario below.

- In Table 1 we have the baseline situation with 5 products being sold, each with different revenue and gross margin %.

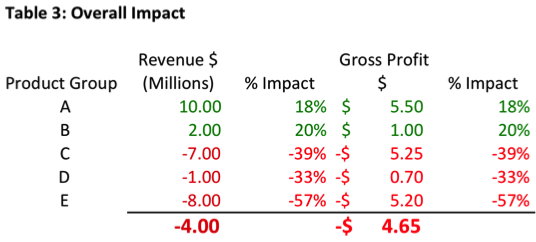

- In Table 2, we see a potential scenario of how that revenue could change with a shared sales force. The new approach works very well for Product A and Product B, which see 18% and 20% revenue growth respectively. The problem comes with Products, C, D and E (which have smaller revenue, but a higher GM% (perhaps due to lower competition, or a developing market). These products see significant revenue decreases and lost margin $.

Table 3 below shows that in this example, the Total Revenue $ Decreases by $4 Million (=96-100) and Gross Profit Decreases by $4.65M ($55.30-$59.95) – not exactly the outcome that the company wanted…

I am not saying that this always happens when companies go to a shared sales force

What I am saying is that companies need to be honest with themselves, recognize that this scenario can happen, and factor this into the decision on how to structure their sales organization

Technology Companies tend to assume that that sales and the product teams will “figure out” a way to minimize this issue, but depending on your situation, the revenue you lose may be gone forever… So how do you know when you are pursuing better sales effectiveness and when you are pursuing an “illusion”?

In next week’s post I will talk about “The Shared Sales Force Checklist”, a tool that I’ve developed to identify when different product groups can be sold together successfully – and when the hoped-for synergy is an illusion…

I welcome any comments below — And make sure you “Follow” our blog (look for the “Follow” link on the upper left) and have your say. I’m also available as a public speaker, to support local and global events in Silicon Valley, or the rest of the flattening world…

For more details, and to stay in touch with this community, contact me or Subscribe to our “Climbing Out of the Box” Newsletter via the form below.

Reps and Channel Not Selling Your Product? Perhaps They Think Selling it Might Be Embarrassing”…

I’ve had this conversation so many times with clients, potential clients and friends – the question is:

Why are the Vendor Reps and Channel Not Selling a Particular Product?

Channel Partners

For channel partners, the answers usually track back to not connecting to how the partners are thinking about selling – and where the product fits This topic was covered in detail in my Channel Not Selling Your Product series of posts, and in particular

- What is the Value Proposition for partners to invest their time in selling your product?

- Is your product and go-to-market program “Channel-Ready”

- What is the Sales Process for selling your product and how does it fit into how your channel partners sell?

Vendor Reps

For Vendor Reps, the challenges have the same root causes, with some different nuances. The bottom line is that they have to sell their companies’ products. But they do have some choices on which products they sell.

Of course they will sell the products where they think they can be successful, but this decision is more nuanced than we might think. Some of the variables that drive this decision include:

- What products are customers asking about (so they can be reactive…)

- Where is competitive positioning the strongest (so they have a high win rate)

- What has the highest deal size (so they can win a few large deals and make money)

- What has the shortest sales cycle (so they can close business this quarter)

- What gets them into the key decision makers in the company (if their job is to sell deep at one or a few accounts)

- The Missing X Factor???

But one key factor is missing from this list. Can you identify it? HINT: Think about human nature and what you personally would do when you are faced with a decision on where to spend your time…

The additional factor I am talking about is:

Where are the Sales Reps (Vendor or Channel) Comfortable Selling?

What drove this home for me was a recent client conversation selling a new technology. I was talking with their Product Marketing folks and we were discussing, “What information does sales needed to be successful selling our product?”

1. The first question to ask is, “What is it they need to do to be successful?”

We quickly agreed that we wanted sales to at least be able to create new opportunities (and that later stages of validation and closing would need specialists anyway). As a context for what we want sales and channel to be able to do, let’s use a basic sales process as shown in Figure 1 below. I talked about this dynamic in detail in my post on the First Natural Law of Enablement –

- Enable Them to Do Something (not to know something)

Figure 1: The Basic Sales Process

2. The second question to ask is, “What information does sales need?” to be successful with Step #1?

I’ve found that that there is clearly a need to focus on the “Why” the product matters to Customers at the front end of the sales cycle, but (somewhat surprisingly) you also need to provide information on “How” a solution works, to serve as “proof” that the solution is real and proven.

But the client’s PMM made an additional point that made me stop and think, as he suggested another key “enablement” need…

3. The third question to ask, and the one this was the “aha moment” for me…

“What information do they need so that they will feel confident enough in their knowledge of the selling context to RISK BEING EMBARRASSED selling your product…”

That is an incredibly important point. How many times have we all seen salespeople steer conversations back to their area of expertise and that they know how to sell. It’s not just a proven track record of success and closed deals. The missing piece is human nature…

Vendor Reps and channel partners will not spend time selling your product if they are not comfortable enough about the customer context, the solution, the products and the overall market that they feel there is a low risk of being embarrassed (which is yet another reason why “Sales Engagement” is the last mile of channel enablement)

I welcome any comments below — And make sure you “Follow” our blog (look for the “Follow” link on the upper left) and have your say. I’m also available as a public speaker, to support local and global events in Silicon Valley, or the rest of the flattening world…

For more details, and to stay in touch with this community, contact me or Subscribe to our “Climbing Out of the Box” Newsletter via the form below.

Channel Not Ready to Sell: Do You Make “Enablement” Real with “On-the Job” Training? (Part 5 of the Series)

A number of my recent posts have focused on challenges and best practices to “enable” your channel and drive revenue. Below is the list of the posts so far:

Channel Not Ready to Sell?

- Part 1 – Perhaps You are Violating One of the “5 Natural Laws of Channel Enablement”? – Outlines these 5 laws and focuses on Law #1: Enabling partners to do something

- Part 2 – 2 Simple Steps to Enable Channel Revenue – Focuses on Law #2 and the need to combine training and tools

- Part 3 – Maybe You Are Training Partners Too Much Like Your Own Sales Reps… – Focuses on Law #3 and the differences between channel training and vendor rep training

- Part 4 – Enablement must be “Packaged” within a Channel Program, To Drive Adoption and Revenue… – Defines packaging and gives examples of how to package enablement to drive revenue

In the final post of the series, we will be talking about Natural Law #5

- Sales Engagement: How Channel Enablement Becomes Revenue $

Let’s start with a baseline question – How much training does it take for someone to be able to do something effectively? That seems like a reasonable question, but it actually misses a critical point of enablement.

- In order to be “enabled” to do something, people need to learn how to do it, and then they need to practice the skills they’ve learned

But think about the “enablement” programs that you’ve seen in your career. How many of them provided opportunities to practice what was learned? I’ve seen it happen it happen occasionally, but not often. Sometimes the vendor coordinates “Role Plays” in a workshop setting, and I’ve done whiteboard training where the participants broke into small groups and practiced whiteboarding to each other. But for many vendors Training = Enablement, because creating “practice” can be complex, hard to measure, expensive and difficult to scale.

That statement defines the dilemma that tech vendors face:

- Partners need practice to be effective selling

- But providing a programmatic way to get practice can be complex and difficult to scale

What can vendors do the provide opportunities to practice and get partners “enabled to sell”. The answer is something that the sales reps do every day – talk to customers (and to do it with partners, as the final step in “enablement”). What I am suggesting is connecting your “Enablement” plan to your Sales Engagement approach.

Those of you working in large vendors may be reading that suggestion with skepticism – how can a field Rep at a complex vendor and a lot of partners (like Cisco or HP) participate in “channel enablement”. After all, that is the Enablement Team’s job and is done by “corporate” folks, leaving the field to do their job, to engage with customers….I see your point, but hold that thought for a second.

When have you seen “enablement” work well, so that the teams in the field are confident that they can rely on the local channel partners to initiate and close sales opportunities?

In my experience, “enablement” works when there is a strong connection between the local sales team and the partners. That connection often occurs in smaller companies where the local sales team has responsibility to recruit and enable partners in their region, to help them in selling deals in their territory (but no so often in larger companies with fragmented responsibilities). Part of the value in this model is that the local sales team feels that they are accountable for helping to “enable” the partners in their region, to help them in selling. But a large part of the value is the local sales team, not only trains the partners, they go with them on sales calls and provide feedback on their progress. In other words, “THEY PROVIDE ON THE JOB TRAINING”.

That sounds wonderful, but it does not scale well to a larger company. You can’t expect the local sales team to own recruitment, on-boarding and the enablement process for all their partners. But the local sales team could be accountable for the “last mile” of enablement, which helping partners practice what they have learned by going after real sales opportunities together.

How would this work? The critical element is creating a channel program requirement that the “last mile” of enablement occur in the field with the local team. In this model, it would be part of their role to work with the partner to jointly engage with customers (and get on-the-job-trainijng). In effect, the process would work the same way it works for the channel-savvy and channel-friendly reps that you already have:

- New partner or newly certified partner calls the local team looking to work together on some opportunities

- Often the onus is on the partner to provide the first couple of contacts for targeting – after all, they have many local customers, just not with the vendor’s product (and what vendor does not want that???)

- As the vendor sales team and partner get used to working together and have some success, the vendor reps bring the partner into opportunities

- As the relationship matures, the vendor sales rep and the partner start to do joint account targeting and selling, with defined roles like “Partner SE runs the POC” follow up from the intial meeting…”

That process is really just basic sales engagement. But for many vendors, this process only occurs where you have sales reps that understand how to work with partners and drive revenue. With channel program design, there are always important details to define and operationalize, but this approach is a winning solution for vendors and for partners.

The opportunity is to build this approach into your channel enablement plan and “Package” the Enablement (see my recent post on this) this into your channel program to scale. This approach has the following benefits:

- Create a set of “enabled” partners who have both the training and experience necessary to help vendors drive revenue

- Help the vendor field standardize on a best-practices sales engagement approach that creates new sales opportunities and a community of enabled partners in their territory

I welcome any comments below — And make sure you “Follow” our blog (look for the “Follow” link on the upper left) and have your say. I’m also available as a public speaker, to support local and global events in Silicon Valley, or the rest of the flattening world…

For more details, and to stay in touch with this community, contact me or Subscribe to our “Climbing Out of the Box” Newsletter via the form below.

Channel Not Ready to Sell? Perhaps You are Not “Packaging” Your Enablement Within Your Channel Program (Part 4 of a Series)

In the last couple of months, I’ve done a series of posts about challenges technology vendors face in “enabling” their partners to sell their products. Below are the posts so far.

Channel Not Ready to Sell?

- Part 1 – Perhaps You are Violating One of the “5 Natural Laws of Channel Enablement”? Outlines these 5 laws and focuses on Law #1 regarding enabling partners to do something

- Part 2 – 2 Simple Steps to Enable Channel Revenue focuses on Law #2 and the need to go beyond channel training, to training and tools

- Part 3 – Maybe You Are Training Partners Too Much Like Your Own Sales Reps… – focuses on Law #3 and the differences between channel training and vendor rep training

This week we will focus on Natural Law #4

- Enablement must be “Packaged” within a Channel Program, To Drive Adoption and Channel revenue…

The first question you may be asking yourself regarding this Law is, “What on earth is “Packaging” (and why is it a Law?)

That is exactly the question one veteran Sales Training/Sales Readiness executive that I worked with asked when he added Channel Enablement to his group’s charter. The first meeting he attended included someone from partner programs, the channel sales executive for the region and a person whose team managed the marketing relationships with key partners.

The new Channel Enablement leader launched into an outline of his vision for a training curriculum – and the rest of the team sat silently. Finally one of the attendees spoke up – “Why would the partners want to take this training and how does it help them get started selling today?” The new channel enablement guy answered with some platitudes on how it would help the partners sell “better”, but it was clear that he did not really get the #1 different between enablement for channels and the sales training program vendors provide for their Reps:

- Vendor Reps MUST sell your products (or they are not around very long) and your sales executives can tell them they MUST do certain things (like take a particular training)

- Channel Partners have other options – and are governed by “Why should I care” If a channel partner, and in particular an individual Rep, SE or Consultant does not see value to them TODAY for your training, you can be assured that they will spend their time somewhere else…

This principle was discussed in detail in my post, “Channel Not Selling Your Products? 3 Questions You Can Ask to Diagnose the Problem.

- Question #1 is “What is the Value Proposition for Partners to Sell your Product?

- And how can they get started making money today…

They key is to get partners to participate in enablement is to think of the situation from their perspective, and use the 2 motivational tools that we humans respond to, “the Carrot and the Stick”. In the language of technology vendor channel programs, the Carrot and Stick translate to

- “What are the Benefits associated with participating in the channel enablement activity/taking provided by the vendor that incent partners to the training?”

- What are the Requirements from the vendor that provide a compelling “stick” to participate in partner enablement?

Let’s illustrate “Packaging” with a specific example

In the period 2008-2012 NetApp created the FlexPod architecture to sell their products with Cisco and VMware – but channel enablement was difficult. The challenge was that the products cut across compute, storage, network and virtualization and was therefore difficult for partners to market, sell and deliver. One partner I talked to during that period said that selling FlexPod was a “6-legged sales call”, because the partner’s staff were siloed with different individuals focused on VMware, Cisco and NetApp technologies, and only a few Reps, SEs and Consultants with sufficient skills to sell and deliver, cross-silo.

Clearly the partners would need to be “enabled”, But creating great training would not be enough – How could Cisco, NetApp and VMware “Package” the enablement, so that partners would participate, and eventually sell more of their solution/products?

A good way to get started on “Packaging” your enablement is to conduct an exercise where your team brainstorms potential “Packaging” options. I’ve found that this exercise gets the item on the agenda and sometimes creates some surprising and successful “Packaging”

- Have a baseline discussion on the partner business model (multiple products, relatively low product margins, need to control costs and maximize selling time)

- Brainstorm potential “Carrots” and the “Sticks” that could have be used to drive participation in enablement (and more sales of your product…)

Then you and your team are in a good position to evaluate the feasibility of these options, and to create the appropriate “Packaging” for channel enablement.

- The Carrot – Potential Incremental Benefits could include things like:

- Exclusivity / Fewer Authorized partners – could limit sale of a product to only the partners that have met enablement requirement.

- Vendors are often hesitant to take this step, but it is a powerful incentive to partners to participate in a program (and often has limited downside because untrained partners will often sell very little of complex solutions anyway and may cause customer sat issues, when they do…

- An incremental margin to partners that complete enablement requirements

- Provide additional discount at Distribution on every sale for partners who meet the requirement

- Provide rebates on qualifying sales, for partners who meet the requirement

- Access to vendor staff that can help the partner sell, such as SEs, Specialists and other staff, for on-site training and sales engagement

- Access to staff can often be the most valuable benefit of all, particularly when it leads to account planning and joint customer engagement.

- However, this benefit can be hard to quantify because vendors often provide vague benefits like named account manager – and partners later find that they are one of 30 partners on their contacts partner list…

- Other benefits – get creative!

- By looking at what it takes to sell your product, you can often find hidden gems that are very important to partners and are relatively easy and beneficial to you as well – but you have to look

- Exclusivity / Fewer Authorized partners – could limit sale of a product to only the partners that have met enablement requirement.

- The Stick – Potential Requirements to Drive Participation in the Enablement could include things like:

- Require partners to complete the enablement to get access to product/solution-specific benefits.

- In the FlexPod example that could mean some number of trained or accredited staff Reps, SEs and Consultants) – to be eligible for the incremental benefits above (discount, access to sell product, etc…)

- Require partners to complete enablement to gain additional program benefits from earning a higher tier in the partner program

- Many vendors have a tiered program, where partners earn “Gold” status based on meeting requirements – and one of the most common requirements is to have a certain number of technical certifications or sales accredited staff

- Require partners to complete enablement to gain the benefits of a specialization or badge in the partner program

- Other Requirements – what do partners really need to do to be successful?

- I often find tech vendors end up listing a series of generic benefits and requirements that are not enforceable, and would have little impact if they were met.

- Ask your team, “what is really needed to be successful” and build this into the Requirements. Maybe it’s a demo center, customer references, certifications in related technologies or even marketing skills – but make the requirements meaningful!

- Require partners to complete the enablement to get access to product/solution-specific benefits.

I’m amazed by how often I see major product launches and detailed enablement plans created by vendors – without really grappling with these questions (and the WIFM for partners). Not surprisingly, vendors don’t get the participation or the revenue impact they expected (and they leave partners muttering to themselves once again that “vendors just don’t understand my business…”)

I welcome any comments below — And make sure you “Follow” our blog (look for the “Follow” link on the upper left) and have your say. I’m also available as a public speaker, to support local and global events in Silicon Valley, or the rest of the flattening world…

For more details, and to stay in touch with this community, contact me or Subscribe to our “Climbing Out of the Box” Newsletter via the form below.